How to Get Help from the District Magistrate for Property Eviction

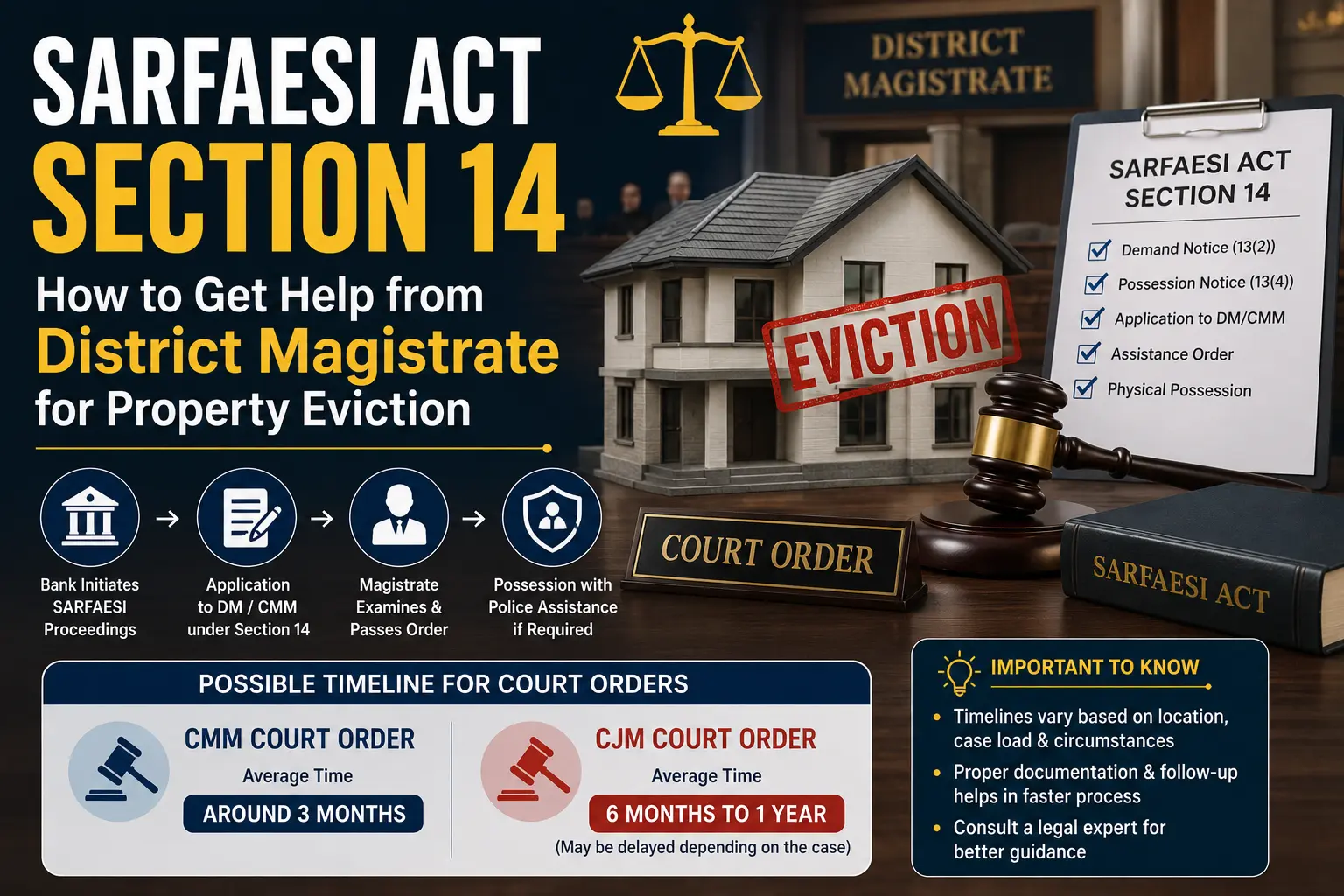

SARFAESI Act Section 14: How to Get Help from the District Magistrate for Property Eviction

One of the biggest challenges faced by banks, auction purchasers, and recovery professionals is obtaining physical possession of a property when the borrower or occupants refuse to vacate. To address this issue, the SARFAESI Act provides a powerful remedy under Section 14.

This provision allows banks and secured creditors to seek assistance from the District Magistrate (DM) or Chief Metropolitan Magistrate (CMM) for taking possession of secured assets and handing them over to the authorized officer.

What is Section 14 of the SARFAESI Act?

Section 14 of the SARFAESI Act empowers the District Magistrate or Chief Metropolitan Magistrate to assist banks in obtaining physical possession of a secured property after the bank has initiated recovery proceedings under the Act.

If the borrower fails to hand over possession voluntarily, the bank can approach the competent authority and request administrative assistance to take possession of the property.

This provision is particularly useful when:

- The borrower refuses to vacate the property.

- Occupants obstruct possession proceedings.

- Physical possession cannot be obtained peacefully.

- Security concerns exist during possession.

Who Can Apply Under Section 14?

The application is generally filed by the Authorized Officer of the bank or financial institution.

The auction purchaser cannot directly invoke Section 14 unless the bank initiates the necessary proceedings. Therefore, buyers should coordinate closely with the bank when purchasing symbolic possession properties.

Role of the District Magistrate

After examining the documents submitted by the bank, the District Magistrate may:

- Verify compliance with SARFAESI procedures.

- Pass orders for taking possession.

- Authorize officers to execute possession.

- Provide police protection if required.

- Facilitate peaceful eviction of unauthorized occupants.

The objective is to ensure that lawful possession is delivered without unnecessary delays.

What Documents Are Usually Submitted?

The bank generally submits:

- Loan documents.

- Mortgage documents.

- Demand notice under Section 13(2).

- Possession notice under Section 13(4).

- Affidavit by the Authorized Officer.

- Details of the secured asset.

- Proof of compliance with SARFAESI provisions.

The authority examines these records before passing appropriate orders.

What Happens After the Order Is Passed?

Once the order is granted:

- Possession execution is scheduled.

- Local revenue officials may be involved.

- Police assistance may be arranged if required.

- Occupants may be directed to vacate.

- Physical possession is taken and documented.

- Possession is handed over to the bank or purchaser as applicable.

Is Police Assistance Available?

Yes. In many cases, police assistance is provided to ensure that possession proceedings are conducted peacefully and without obstruction.

However, police assistance is generally provided pursuant to the Magistrate’s order and applicable procedures. Buyers should avoid attempting self-help eviction methods.

District Magistrate vs Chief Metropolitan Magistrate

Depending on the location of the property, applications may be filed before:

District Magistrate (DM)

Typically applicable in district jurisdictions outside metropolitan areas.

Chief Metropolitan Magistrate (CMM)

Applicable in metropolitan jurisdictions where such authority exists.

The competent authority depends upon the location of the secured asset.

Practical Timeline: What Buyers Should Expect

Many first-time auction buyers assume possession will be handed over immediately after the auction. In reality, possession timelines can vary significantly.

Based on practical recovery experience, proceedings through the Chief Metropolitan Magistrate (CMM) may sometimes be completed within approximately 3 months in straightforward cases.

However, matters involving District Magistrate or Chief Judicial Magistrate processes can take considerably longer depending on workload, local administration, objections, documentation requirements, and court-related delays. In some cases, possession proceedings may take 6 months to 1 year or even longer.

Buyers should therefore consider potential possession timelines before bidding on symbolic possession properties.

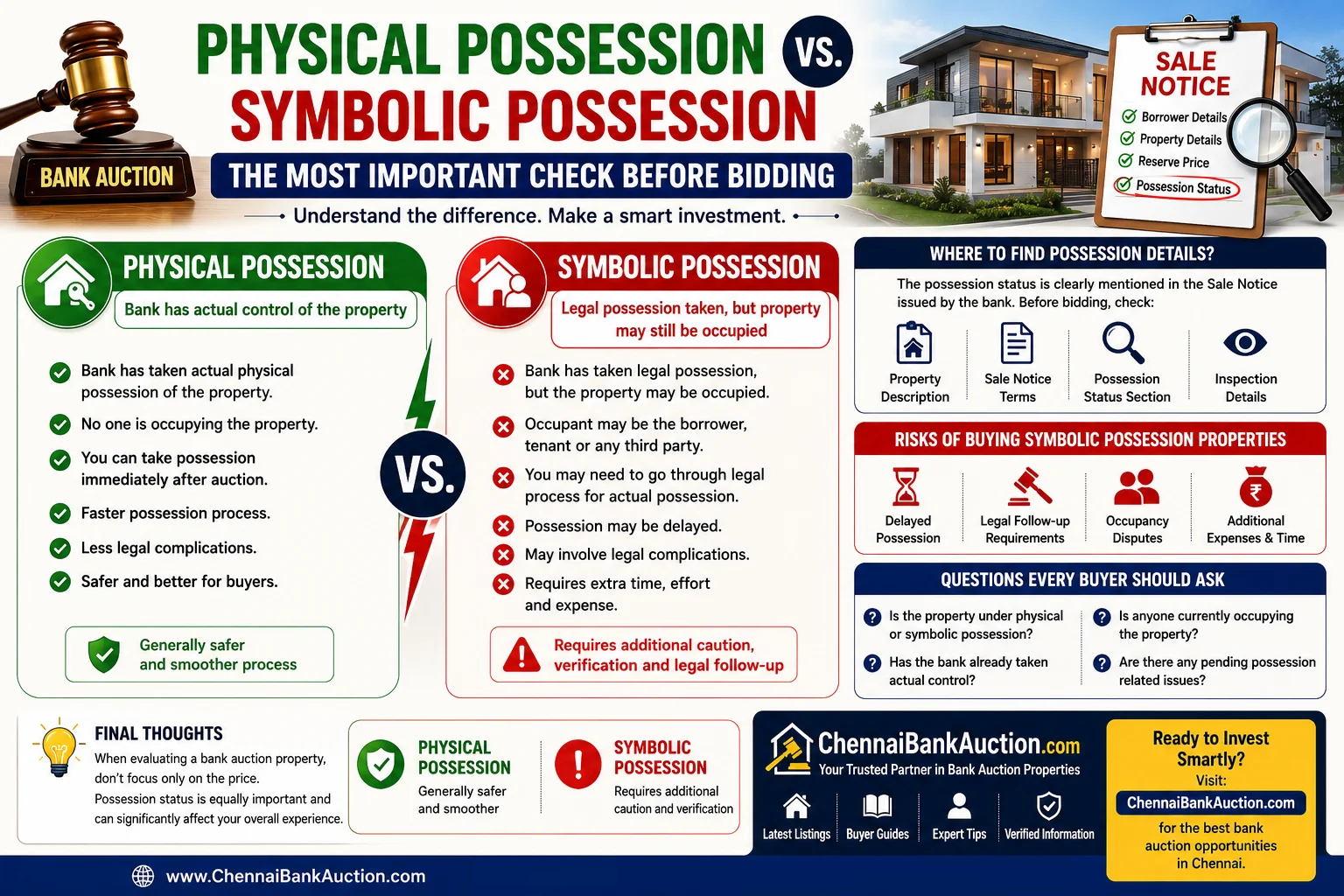

Why Many Investors Still Buy Symbolic Possession Properties

Despite the waiting period, many investors actively participate in symbolic possession auctions because:

- Properties are often available below market value.

- Competition is usually lower.

- Better discounts may be available.

- Higher long-term returns are possible.

- Some properties attract very few bidders.

Investors who understand the possession process often view the waiting period as part of the investment strategy.

Precautions Before Bidding

Before purchasing a symbolic possession property:

- Verify possession status carefully.

- Read the sale notice thoroughly.

- Understand potential legal timelines.

- Consult a property lawyer.

- Speak with the bank regarding possession proceedings.

- Budget for legal and administrative expenses.

- Avoid unrealistic expectations regarding possession dates.

Conclusion

Section 14 of the SARFAESI Act plays a crucial role in helping banks obtain physical possession of secured properties when borrowers refuse to cooperate. Through the assistance of the District Magistrate or Chief Metropolitan Magistrate, possession can be lawfully secured and delivered.

For auction buyers, understanding the Section 14 process is essential, especially when purchasing symbolic possession properties. While possession may take time in some cases, investors who conduct proper due diligence and understand the legal process can often secure valuable opportunities through bank auctions.

Share with your friends

Recent Posts